If I Pay My Credit Card Can I Use It Again

Citi is an advertising partner

Whether you lot've been using credit cards for years or you're applying for your beginning 1, they can be confusing. Depending on how you utilize them, credit cards can either exist incredibly dangerous or immensely helpful. This guide will walk you through what you need to know nigh using a credit menu, edifice credit and earning rewards.

How to use a credit card: The 4 principles to master

You should always handle credit cards with extreme intendance. Unlike debit cards, you're making purchases on credit — meaning yous're 100% liable for paying back everything yous charge to your credit card. If you aren't careful, you can end upward in a lot of debt.

At that place are four primary principles to condign a credit card master. If y'all accept abroad anything from this guide, you should always follow the first rule — pay your pecker on time and in full every single calendar month. This strategy lonely will assist your personal finances tremendously.

If yous'd like to larn other means to maximize your credit bill of fare use, read on for the best practices for managing your credit bill of fare.

Rule #ane: Always pay your bill on fourth dimension (and in total)

The near of import principle for using credit cards is to always pay your neb on fourth dimension and in full. Post-obit this unproblematic rule can aid you lot avoid interest charges, late fees and poor credit scores. By paying your bill in full, you'll avert interest and build toward a loftier credit score.

The consequences of missing a payment

By consistently missing payments, yous could finish up paying hundreds of dollars in late fees. The negative consequences spiral — once your credit score takes a hit, you could face thousands in interest when applying for futurity mortgages or loans. If you're unable to pay your beak on time, information technology may be fourth dimension to cut up your carte du jour.

You're normally given multiple options to pay your credit card statement each month. While it may be tempting to pay merely the minimum payment — which could exist as depression as $25 — you'll start to accrue interest, leading to years of debt. The all-time practice is to pay off your credit menu nib as soon equally you make a purchase. This way, you tin get into the habit of paying your bill long before its due appointment.

Each month, your issuer will provide your credit carte du jour statement with 2 dates: the closing date and payment date:

- The closing date is the terminal twenty-four hour period yous tin make a charge for a monthly statement. Subsequently the closing date, whatever new transaction volition become onto next month's statement.

- The payment date tells you when the payment for a detail argument is due.

In the example above, this user has a closing date of Jan. 16 and a payment date of Feb. 13. This monthly statement ran from Dec. 17 to January. 16, with a payment due on Feb. 13. In this case, you have a 28-24-hour interval grace period after your statement appointment before you lot're required to make a payment. Y'all won't be charged any interest during this grace period as long as you pay in full by the due date.

All credit cards are dissimilar and volition have varying billing cycles, payment dates and grace periods. Review the information for your credit card to understand how it works for your situation. If you're having trouble remembering to pay your bill, most issuers will allow you lot to gear up automated payments or schedule reminders each calendar month.

Rule #two: Continue your balances low by only charging what you lot tin afford

In addition to making on-time payments, it'south essential to keep your balance low relative to your available credit limit. There are 2 main benefits to maintaining a pocket-sized residual:

- Depression balances help increment your credit score.

- You're more than probable to pay off your residue in full and on time.

Many factors decide your credit score, simply a significant portion (30%) comes from credit utilization. In other words, this is the ratio of what you owe to your total credit limit. For case, if you have a credit limit of $ane,000 and charge $500 to your card, your credit utilization would exist 50%.

While there'southward no clear definition of your credit utilization, experts believe that you should keep it under 30%. Annihilation higher than that can decrease your credit score. To reach a low credit utilization ratio, yous should typically charge less than you tin afford. By keeping a low balance, you minimize the chance that you'll spend more you can pay off at the end of the calendar month.

Finally, don't view your credit carte du jour as an extension of your budget. You should never charge more than what you can currently cover in your banking company business relationship. Information technology'due south tempting to spend ahead based on what y'all know you lot'll go paid, merely it's a bad practice. If you lose your chore or run into an emergency, you won't be able to cover those charges. People don't intend on having credit card debt — it builds slowly and becomes a vicious bike that becomes hard to break.

Dominion #3: Understand how interest is calculated

Contrary to popular belief, interest isn't calculated based on the remaining balance subsequently making a minimum payment. In reality, issuers calculate interest based on your average daily residue, calculated past taking your carte's Apr (Annual Per centum Rate) and dividing this number by 365.

For case, assume you have a statement balance of $ane,000 and make a payment of $800 on the due engagement. You'll be charged interest on the remaining balance of $200 and lose your grace period. In the new billing cycle, any transactions will begin accruing involvement immediately. The grace period where no interest is charged but applies if you pay your residuum in full past the payment appointment.

Rule #four: Monitor your monthly argument

Monitoring your argument helps you check for fraud, stay on a upkeep and maintain a low rest. Fifty-fifty if you've ready an automatic payment, it's even so wise to log in and check your statement every calendar month to ensure there are no suspicious transactions.

Thankfully, most issuers have sophisticated technology that checks for fraudulent charges, but they may not grab them all. At least once a calendar month, you should check your statement and verify there aren't any purchases you don't recognize.

In addition to checking for fraudulent activity, monitoring your statement will help you stay on budget. There's no fashion to know if you're maintaining a depression balance, keeping your spending in check, or bravado the upkeep unless you lot're regularly checking in.

How to apply a credit card to build credit

As the proper name suggests, credit cards are i of the foremost tools for building a credit score and can make a great foundation for your credit history. The best way to build your score using credit cards is to follow the recommendations listed above: Pay on time and in full, and keep a low residue. Beneath, you'll learn how credit scores are calculated and exactly how credit cards affect them.

Know how your credit score is calculated

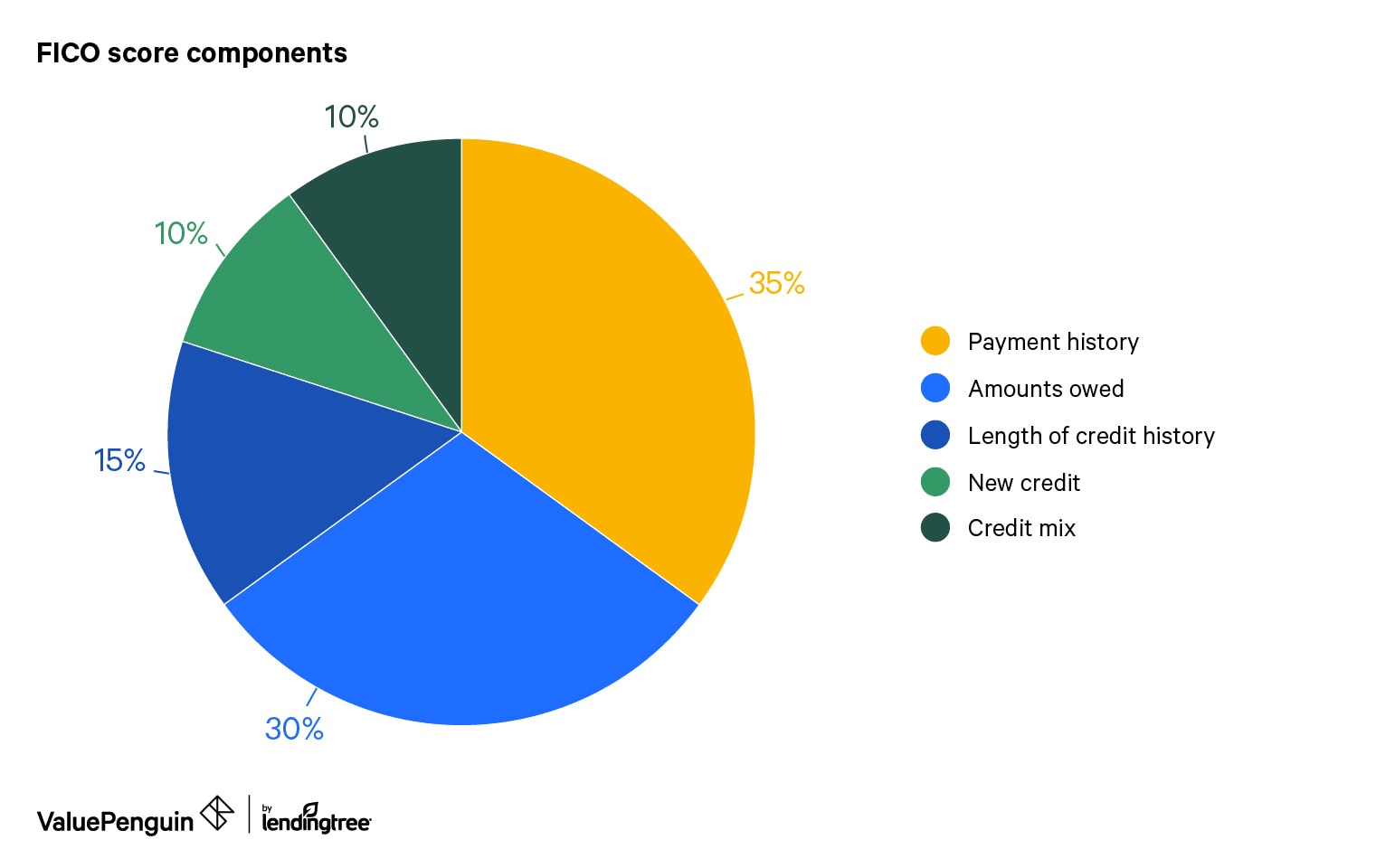

The FICO Score is the most usually used credit score that well-nigh lenders refer to and is fabricated up of five cardinal components:

- Payment history is determined by how oft you pay on time and how reliable you are as a borrower.

- Credit utilization is the ratio betwixt how much you borrow (balance) to how much is available to y'all (credit limit).

- Length of credit history is how long you lot've used credit — the longer, the ameliorate.

- New credit is how frequently yous apply for credit products or loans, and what per centum of your credit comes from recently opened accounts.

- Credit mix is how many unlike types of credit you use.

FICO Scores range from 300 to 850, and the average score is 701. It takes time and patience to build your credit score. Since the length of credit history determines fifteen% of your score, it'southward a adept idea to get-go early on and learn how to manage your credit properly.

Other strategies to help you build your credit score

Payment history and credit utilization brand up 65% of your score. Because these two factors lone incorporate the majority of your score calculation, you should maintain a low balance and never miss a payment to beefiness up your score. If y'all're already following these principles, hither are 4 more strategies to aid you lot build your credit score:

- Never cancel your first credit card. Unless information technology has an annual fee, you desire to go along your oldest line of credit as long as possible, as this will help your average account age.

- Ask for a credit-limit increment, but don't increase your spending. Call your credit carte visitor for a credit-limit increment if y'all want to reduce your credit utilization ratio. This tactic will help your utilization score by decreasing your ratio.

- Open a new credit card and so set a recurring neb and automatic payment to that card. Setting up this small recurring payment (such equally a streaming subscription) will help both your overall utilization and your payment history.

- Pay off all your credit cards a few days before each argument closes if you're applying for a loan soon. Paying off your cards early volition decrease your overall utilization and heave your credit score for a few days.

How to use a credit carte to earn cash dorsum and rewards

Earning rewards from a credit card is the fun function. But kickoff, you should consider what your height spending categories are, then pick a card that volition provide the all-time returns for y'all. Everyone's spending habits are different — some people may spend a lot on travel, while others only spend on groceries or takeout.

Analyze your spending habits to maximize your rewards

Take a look at the past few months of your spending and categorize it as all-time you tin can. Ask yourself the following questions: Do you spend a lot on gas and groceries? How often practise you travel? Can you lot put work-related purchases on a credit card and then go reimbursed by your visitor?

Once you figure out which categories you're spending the almost in, start researching different credit carte du jour options that fit your needs. Later analyzing your spending, you may discover that you want to use two credit cards to maximize rewards. All the same, while juggling cards tin can assistance you earn more rewards, don't get so distracted you end up spending more than you usually would.

Sympathize cash back vs. points vs. miles

Adjacent, y'all should consider which types of rewards you're looking for. In that location are three main types of rewards currency: greenbacks back, points and miles. Information technology may make sense to earn points and miles through travel rewards cards if you similar to travel. If yous adopt to earn cash rewards, await at cashback cards instead.

Credit card rewards tin be disruptive, and most credit cards have restrictions on how you tin redeem the rewards. For case, some cards require a minimum redemption threshold, or yous may take to wait multiple billing cycles to receive your rewards. Consider how much time and effort you want to put in versus getting a unproblematic card with straightforward options.

Beneath, we've hand-picked our favorite beginner rewards credit cards that are easy to employ and offering excellent returns:

| Menu | Best for... | Annual fee | Rewards rate |

|---|---|---|---|

| Hunt Sapphire Preferred® Card | Travel rewards | $95 | 5x on travel purchased through Chase Ultimate Rewards®, 3x on dining and 2x on all other travel purchases |

| Citi® Double Greenbacks Menu – 18 month BT offer | Cashback | $0 | Earn ii% on every purchase with unlimited ane% cash back when y'all purchase, plus an boosted i% as y'all pay for those purchases. |

| Hunt Freedom Flex℠ Card | Rotating categories | $0 | 5% greenbacks back on up to $1,500 in combined purchases in bonus categories each quarter you activate. Enjoy new 5% categories each quarter! Plus, earn five% cash dorsum on travel purchased through Hunt Ultimate Rewards®, 3% on dining and drugstores, and ane% on all other purchases. |

ValuePenguin'south verdict

A credit card can make or interruption your financial future. If used correctly, you lot'll enjoy a plethora of benefits, from a peachy credit score to valuable credit carte du jour rewards. All the same, if you fail to manage your credit card responsibly, you may find yourself spiraling out of control and into debt. Knowing the bones principles of using a credit card can avoid the latter outcome entirely and secure a promising outlook for your personal finances.

Source: https://www.valuepenguin.com/how-use-credit-cards

0 Response to "If I Pay My Credit Card Can I Use It Again"

Postar um comentário